From Team Nationals to Team Europe for digital connectivity

Summary

The Global Gateway's success depends on meaningful private sector engagement, which the EU hopes to facilitate via the 'Team National' framework. The Team National aims to unite a member state's private sector with its economic ministries, development agencies, and financial institutions to support internationalisation. Team Nationals are essential for creating a unified ‘Team Europe’. However, aligning these national approaches with one another and with EU policy remains a key challenge.

This briefing note examines the digital connectivity offers of France, Germany, Finland, Sweden and Italy. France has the broadest industrial offer, especially in the subsea and space sectors, supported by the robust AFD Group, but could benefit from broader European support. Germany, while strong in digital diplomacy and cooperation through GIZ, struggles to mobilise financing for the digital sector despite the size of the KfW Group. Finland and Sweden prioritise technology and have focused their offers around key companies and small and medium enterprises. Italy, a newcomer building its Team National through the Mattei Plan, is in the early stages of developing its cooperation tools and financing for digital sector engagement.

Developing a truly effective ‘Team Europe’ approach faces obstacles, including varying speeds of Team National development, fragmented institutional setups, and difficulties in coordinating development agencies and financial institutions. Private sector actors also struggle to understand how to engage with the Global Gateway strategy. To improve, member states need to create authority and budget for Team National coordination, while at the EU level, there is a need for simplified coordination mechanisms, making the Global Gateway Investment Hub more user-friendly, and piloting new mechanisms for building transnational consortia to support SMEs and smaller member states.

Introduction

The success of the Global Gateway will depend on meaningful private sector participation. Yet there is no ‘EU’ private sector. Many European private sector actors remain anchored in their domestic markets. Member state institutions thus have an important role to play in making their private sectors aware of the financial and non-financial measures available to support internationalisation, both at the national and at the EU level. The EU institutions are currently encouraging member states to develop a national approach through the ‘Team National’ framework, bringing together the private sector with economic and external-facing ministries, development agencies, export-credit agencies, public development banks and development finance institutions. This national engagement is particularly vital in bringing on board small and medium enterprises (SMEs), which are often organised within national trade associations.

The Team Nationals are also the basis for building one unified Team Europe, and this unity is also central to Europe’s value proposition. It is also vital to create space for smaller EU member states to participate in the tech business offer. The Global Gateway Investment Hub was created to allow Team Nationals to submit project proposals, but for smaller member states that are dominated by SMEs, it will be important to develop joint projects that may involve a number of smaller private sector actors. Yet aligning Team Nationals with one another and with EU policy remains a challenge.

The following briefing note offers a deep dive into several EU member states that are central to beginning to operationalise the Tech business offer. France has the broadest industrial offer on digital connectivity, while Germany yields the widest range of diplomatic and cooperation tools. Finland, and more recently Sweden, have forged their digital offer around leading companies in the sector, mostly their mobile network suppliers, but also have thriving SME sectors. Italy was chosen as a newcomer with a substantive industrial base and the ambition to play a bigger role in global digital connectivity, especially in Africa.

This briefing note is part of a four-part series on digital connectivity in the European tech business offer. The other three parts of the series explore the role of sovereignty in EU international digital policy; the European industrial connectivity offer; and the evolving European toolbox around international digital connectivity.

These policy briefs draw on a targeted review of publicly available literature and programme documentation, as well as on approximately 40 semi-structured interviews with stakeholders, including those from public institutions, development partners, private companies and civil society. In addition, the authors participated in the D4D Connectivity Working Group in December 2026, which included presentations and comments from many stakeholders.

France

France has the most cross-cutting industrial offer on connectivity, marked by a strong strategic interest in the subsea and space sector, but also by a rich SME landscape fresh from participation in the rollout of Europe’s most ambitious fibre rollout programme, Le plan France Très Haut Débit (PFTHD). It is gradually developing a strong digital offer as part of its Team National, building on its relatively strong domestic digital infrastructure industry and history of engagement in international infrastructure projects, notably in Africa. Yet, a number of actors mentioned that France’s strained relationships with certain countries in Africa can make it more difficult for French private sector or development actors to engage or to be seen to impose constraints, for instance around ‘trusted connectivity’.

France does not have a separate digital ministry, and digital policy falls under several ministries, with infrastructure largely under the Ministry for Economics, Finance and Industrial and Digital Sovereignty. The powerful cybersecurity agency, ANSSI, reports to the Prime Minister’s office. Further, France encounters reputational issues in parts of Africa, and has sometimes struggled to convince European partners that it is a team player - perhaps highlighting the fragmented nature of its digital diplomacy.

While the Employers Association, MEDEF, is the coordinator of the overall Team France, France has also created a ‘Strategic Sector Committee for Digital Infrastructure’. It brings together four trade associations that represent a large number of companies whose value chains extend from cable manufacturers to equipment manufacturers and installers to telecom operators (1). The Committee includes a working group on internationalisation that developed a catalogue compiling the French international offer.

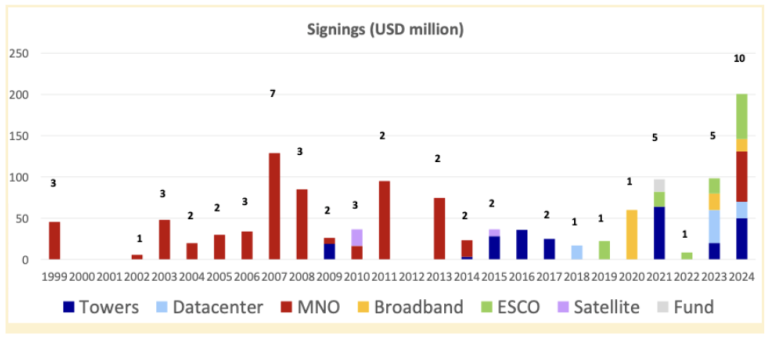

France’s two experienced development finance institutions, AFD and Proparco, and its cooperation agency, Expertise France, which together make up the AFD Group, with a unified digital strategy, have each developed considerable digital expertise as they have expanded their focus on the sector in recent years. Both AFD and Proparco previously had access to sufficient domestic financing from the French government, allowing them to scale up their lending to the digital sector without necessarily accessing European funds. The digital sector represents approximately 10% of AFD Group’s portfolio overall. AFD has been particularly active in the submarine cable sector, notably spearheading extensions of the Ella-Link cable, but is also active in terrestrial fibre. Although there is good communication within the AFD group, practical cooperation between AFD and Proparco is complicated by the very different needs and timelines for funding in the sovereign and private sector segments of the market. Proparco has greatly increased its lending to the digital sector, which now represents a sizable proportion of its portfolio and covers the whole range of submarine cables, fibre, 5G connectivity and data centres (see below).

Figure 1: Proparco’s track record of financing digital infrastructure (1999-2024)

The French financing ecosystem has traditionally been characterised by a strong emphasis on sustainable development, underpinned by robust climate criteria. It has also had a focus on untied aid and strong partnerships with international banks, notably IFC, World Bank and the Inter-American Development Bank (IDB). Yet, there are clear shifts underway in the French policy environment. France’s strong support for a European preference in EU procurement appears to affect the domestic approach to development finance. Multiple sources noted that the AFD Group is in the process of developing a new strategy, with a much stronger focus on engaging the French private sector. It also appears likely that the group will expand its traditional focus on Africa to a stronger engagement in Latin America and the Caribbean and Asia-Pacific.

Expertise France plays a complementary role to that of the French and European DFIs. Unlike most of its European peers, its focus extends beyond development cooperation, and its reach is global, with the capacity to work even in Europe. This allows it to facilitate discussions on public policies for investment by drawing on France’s own experiences with developing connectivity plans with regulators and local councils. It is also able to actively engage with the private sector, which it has been actively doing, notably for the Asia branch of the D4D Hub.

France undoubtedly has the strongest cross-cutting offer with regard to digital connectivity that has been well developed by its domestic industry. It also benefits from a strong cooperation apparatus in the shape of the AFD Group. Yet, by working together with the EU institutions and other member states, France could benefit from a more cross-cutting European economic diplomacy and financial firepower.

Germany

Germany lacks the firepower of France on international digital connectivity, with no industrial equivalent of the scale of ASN, and no mobile or satellite communications operators with a substantive presence in the Global South. Nor can it match France’s well-organised SMEs in the high-speed broadband sector. Within the core digital sector, Germany’s strength lies in services – through software companies like SAP, but also through SMEs with data-driven solutions for earth observation, manufacturing or e-government.

Yet German stakeholders interviewed view a coherent and competitive offer for global digital connectivity as in the European strategic and economic interest. For one, under Global Gateway, German companies such as Siemens offer cross-cutting engineering or energy solutions for digital infrastructure. Secondly, German industry representatives have argued that European-built digital connectivity infrastructure would benefit German business interests in other sectors.

The digital sector, which is relatively fragmented in Germany, has not seen a high level of public-private coordination. This may be changing with the growing recognition that the digital transformation is a precondition for the future competitiveness of German industry, but also for a modern government and society. The Federal Ministry for Digitalisation and State Modernisation (BMDS)is in charge of Germany’s international digital policy, multilateral governance processes at the UN level and dialogues with partner countries. The Federal Ministry for Economic Cooperation and Development (BMZ) sets policy guidelines and provides funding for Germany’s digital cooperation agency GIZ, although the future level of engagement is currently under review.

Germany’s unique institutional setup can at times lead to a mismatch of perspectives in European conversations, but the country has been among the most active in engaging with Team Europe. The German development agency, GIZ, has launched many flagship digital projects in partner countries and regions, such as the Digital Transformation Centers in Africa. GIZ was an early supporter of a Team Europe approach to digital cooperation, co-founded the D4D Hub, and works closely with EU Delegations in many parts of the world.

For the purposes of feeding project proposals into the new investment hub, the BMZ coordinates with two other ministries. The Federal Foreign Office (AA) is in charge of the political steering, and the Federal Ministry for Economic Affairs and Energy (BMWE) has the instruments to support German companies in international markets. A unique German instrument combining cooperation and investment instruments for all sectors is the Agency for Business and Economic Development (AWE). A collaboration between GIZ and the development finance institution DEG, the agency advises companies in accessing development cooperation and finance instruments. The AWE currently does not place a strong focus on the digital sector and has been subject to staffing cuts, but the growing focus on the private sector in cooperation may lead to a reversal of this trend.

German industry and business associations, such as the BDI and the digital association Bitkom, provide input for Germany’s international digital policy. Unlike the specialised digital infrastructure associations in France, Bitkom is a crosscutting digital industry association, and about half of its 2,200 members are SMEs from the software sector. Its wide range of members includes most major US and Chinese tech companies through their German subsidiaries.

Germany’s financial institutions for development, under the roof of its public development bank, the KfW Group, contribute to financing Europe’s international digital investments. The KfW Development Bank extends sovereign loans and grants on behalf of the German government. In contrast with France’s AFD, it does not have a dedicated team for digital connectivity, but integrates digital investments across existing sectors such as energy, education or health. This reflects Germany’s domestic industry focus, but complicates co-financing digital projects with other European DFIs. KfW Group’s private-sector arm DEG, on the other hand, has steadily increased its digital investments, working closely with EBRD and its French and Finnish equivalents, Proparco and Finnfund, for instance, on a co-investment in IPT Power Group (See the accompanying briefing note Karaki et al. 2026 for more). The third KfW subsidiary, the IPEX-Bank, supports German and European companies through project and export finance, with a focus on Asia. Unlike investors in France, Finland or Sweden, which follow their own digital infrastructure companies into global markets, the KfW Group has struggled to find German projects for its digital infrastructure pipeline, especially when it comes to riskier markets such as in Africa.

Despite its impressive track record on digital diplomacy and its omnipresence in the digital cooperation sector, Germany struggles to provide financing for the digital sector. Considering the size and financial firepower of the KfW Group, which is second only to the EIB, Team Germany could make an important difference in financing digital connectivity if it could mobilise its private sector as part of a broader European approach.

Italy

Italy is a relative newcomer to international digital cooperation, but has been actively engaged in building its Team National since the launch of the Mattei Plan, its international investment strategy for Africa, in 2024. Although not initially a pillar of the Mattei Plan, digital transformation was included following consultation with partners. Italy’s G7 Presidency in 2024 also marked an important uptick in Italy's global engagement on digital topics, including through the launch of the AI Hub for Sustainable Development with UNDP and private sector partners. However, despite strong political buy-in, the Italian approach is still in the early stages of development. Indeed, as with Global Gateway, the Mattei Plan currently combines a number of existing projects that have been relabelled under the Mattei Plan, and several pilot projects that may be scaled with time.

The Mattei Plan is coordinated by the Prime Minister’s Office, while the evolving Team National approach is being coordinated by the Ministry of Foreign Affairs, involving sometimes complex coordination. Meanwhile, several flagship projects like the AI Hub and the Blue-Raman cable are coordinated by the Ministry for Business and Made in Italy. The cooperation section of the Ministry of Foreign Affairs coordinates many cooperation projects, including its efforts to develop a pipeline of bankable projects under the ‘Digital Flagship’.

As the main implementing partner, UNDP Italy works closely with Italian ministries and plays a key role in Team Italy’s ambitions to scale up its digital engagements in Africa. It is in the lead both on the AI Hub for Sustainable Development and on the Digital Flagship. Meanwhile, the Italian development agency, AICS, is a member of the D4D Hub and is exploring avenues to increase its own engagement on digital topics. Cassa Depositi e Prestiti (CDP) is the Italian public development bank, but it only became a development bank in 2015, and its experience in the area of international cooperation is thus relatively new. At the time of writing, CDP had not yet engaged in any international investments in the digital sector.

Italy has the basis to be an important player in the EU’s offer on digital connectivity. It is very much in the early stages of developing its cooperation tools and financing mechanisms for the digital sector. Yet, it has shown political willingness to engage and play a role.

Finland

Finland invested in building Team Finland starting in the 2010s and has strongly prioritised digital cooperation within the Global Gateway. There is a cross-cutting focus on technology in Finland’s foreign and security policy, as well as in its international trade and development policy. The Ministry of Foreign Affairs has compiled Finland’s international technological priorities across domains - security, economic, governance and cooperation, and brought together relevant staff working on digital policy from different perspectives in the Unit for Technology and Sustainability.

Team Finland has, from the outset, represented not only the interests of the national champion, Nokia, but also sought to bring in SMEs, particularly in the cybersecurity sector. This was highlighted by a Non-Paper ‘Global Gateway: Proposals for effective implementation’ that Finland and Estonia prepared and presented in the Council of the EU’s Working Party of Foreign Relations Counsellors (RELEX) in March 2024, and again in the Foreign Affairs Council that gathered ministers responsible for development policy in May 2024.

Finnfund became the first European DFI to sign and deploy a €100 million EFSD+ open architecture (i.e. private sector) guarantee for the digital sector. The resulting Africa Connected programme was expanded to €222 million in 2025 and given a global scope. Finnfund signs an average of approximately €200 million of new investments per year, with the digital sector representing about 40%. Among European DFIs, Finnfund stands out for taking on projects with a relatively small ticket size in the low millions (See accompanying briefing note Karaki et al. 2026). While its clients are generally local businesses in developing countries, it works with the rest of Team Finland to build opportunities for international clients to engage with Finnish or other European partners. In addition to its role within Team Finland, Finnfund is esteemed by other European DFIs for its work in pipeline development and its openness to working with other European and global partners - whether financiers or industry actors.

To this end Finnfund coordinates closely with the export credit agency Finnvera, which plays a key role in the Finnish digital ecosystem and which plays a key role in positioning Finnish companies such as Nokia as preferred partners for local businesses. Finnvera, for instance, supported Nokia’s operations in India through a € 1.5 billion guarantee.

Finland’s HAUS, a public company that has traditionally supported domestic public management, is also a very active member of Team Finland in the digital sector. It plays an important role within the Connectivity working group at the D4D Hub, and takes part in several digital sector Team Europe initiatives, including working with GIZ to implement the Digital Investment Facility (DIF)(See accompanying briefing note Karaki et al. 2026).

With its crosscutting international technology team, its growing focus on digital cooperation and financing, and its strong Team Europe spirit, Finland has led the way in developing the Team National digital. With time, Finnfund might even begin to play a more pan-European role in supporting projects that originate from other EU member states.

Sweden

Team Sweden is also relatively advanced in combining policy engagement, development cooperation and financial instruments. In 2024, Sweden released a strategy for foreign and security policy on cyber and digital issues, in a digital world that emphasises the critical importance of connectivity, networks and information. The competitiveness of Swedish businesses is directly linked to ‘well-functioning connectivity’, and it highlights the significance of one of only a few ‘trusted suppliers’ research activities being concentrated in Sweden. Business Sweden plays a key role as the coordinating entity of Team Sweden, helping mobilise and facilitate Swedish private sector engagement, and could be highly relevant for Swedish digital SMEs.

To date, the Swedish DFI Swedfund invests indirectly in some digital infrastructure through funds, but most of its investments focus on digital services and/or mainstreaming digital technologies across other key sectors (e.g. financial services). This limits downstream opportunities for the Swedish digital private sector, which could be involved through Swedfund clients’ public procurement process. That said, as of 2025, Swedfund can now invest in the digital sector (including in infrastructure through debt and equity products) in middle-income countries - something it could only do exceptionally in the past, and that could unleash new opportunities. In addition, while Swedfund is one of the only Swedish institutions - besides SIDA - that can access EFSD+ blending and guarantees from the EU, this has not materialised into concrete direct investments in the digital sector, let alone trusted connectivity.

The Swedish export credit agency, EKN, is a key institution supporting Swedish digital companies’ internationalisation. Given its nature as a state agency, EKN suffers to a more limited extent from traditional issues other ECAs face, such as country exposure (which limits the amount of financial support that can be provided to Swedish exporters). EKN recently launched a new soft finance/tied aid instrument for large infrastructure projects. Yet, as with other ECAs, it cannot cover all types of risks and/or to the full extent, such as local currency risks, which are one of the issues affecting exporters that ECAs alone cannot mitigate.

Swedish development agency SIDA focuses on developing capacity and institutions, but also has a guarantee mechanism for the private sector to mobilise capital for developmental projects. It has a portfolio of about €20 million focused on connectivity, including support to the ICT Policy & Regulation (IPRIS) project, the World Bank Trust Fund for Digital Technology, GSMA and the Association for Progressive Communications (APC). SIDA’s focus is moving away from long-term advocacy activities towards a stronger focus on developing capacity and institutions, with the overarching goal of inclusive connectivity and inclusive services.

Sweden has all the ingredients for a successful Team National digital, and notably benefits from EKN’s role as a state agency. Yet, Sweden still struggles to provide an integrated toolkit for funding digital infrastructure projects in developing markets.

Building Team Europe

Team nationals have a key role to play, but many European stakeholders still argue that there is a need for a genuine Team Europe approach to financing and private sector engagement, bringing the team nationals together to develop projects at scale. As previously mentioned, this is a particular concern for smaller member states that have potentially interesting solutions, but cannot develop Global Gateway initiatives singlehandedly.

The D4D Hub was founded as an incubator for Team Europe Initiatives (TEIs) in the area of digital transformation, and has made trusted connectivity one of its key pillars, with a working group focused on this topic. The Digital Diplomacy Network, meanwhile, convenes policy discussions around international digital policy. The Association of European Development Finance Institutions (EDFI) and Joint European Financiers for International Cooperation (JEFIC) also have a role to play. Yet, it appears that there is still work to do to ensure that these mechanisms are able to operate successfully and carry out their functions successfully, notably in areas such as information sharing, facilitation and project development.

The D4D Hub was initially established by member state development agencies with a strong focus on building TEIs in the international cooperation domain, and with a strong focus on European values. Its Secretariat continues to be staffed largely by the development agencies, but its mandate is unclear and subject to competing demands from the European Commission and Member states. The focus of the Hub appears to be shifting in line with European Commission and member state priorities, with a growing focus on private sector engagement as evidenced by the 2025 D4D Exchange Days, the D4D Hub’s flagship annual event for members. Yet the competing demands and complex governance of the Hub get in the way of it fulfilling its potential.

EIB and EBRD form the bedrock of the Team Europe approach, given their scale and also the fact that all member states are shareholders. Yet there is also an important role for smaller financial institutions in development in the member states to play in a truly Team Europe approach. These institutions have very complementary roles given different ticket sizes (See accompanying briefing note Karaki et al. 2026), but this does not yet function as smoothly as it might. Furthermore, given that some member states do not have DFIs or PDBs, important questions arise about whether an institution based in one member state can engage with and build projects that support the interests of the private sector in another member state.

Aside from the D4DHub and the support that European multilateral development banks like the EIB and EBRD can provide, the European Commission has developed the Global Gateway Investment Hub, which provides a framework for engaging the European private sector in Global Gateway. The investment hub allows the European private sector to submit investment proposals to their Team Nationals, which in turn can request support from the European Commission. The objective is for the EU to provide additional support to what Team Nationals can offer. Yet, small member states raise many issues with the focus on the Team National approach, highlighting that they lack the resources or a sufficiently large private sector to support proposals alone. This suggests that mechanisms to develop joint projects and submit jointly to the Investment Hub are missing at present.

There can also be difficulties in getting various types of actors to work together, both at the national and particularly at the European level. For instance, while development agencies traditionally work on helping develop conducive business environments, they do not necessarily engage with DFIs to align their programmes' focus to DFIs' needs in a way that would unlock investments. As a result, some DFIs are engaging in policy dialogue, doing similar work as a development agency and competing for donors’ resources. Likewise, while many development agencies are increasingly working on developing a pipeline of private sector projects for financing, as with the DIF previously mentioned, financial institutions for development are often sceptical about the ability of non-financiers to prepare bankable projects.

Whether via Team National or Team Europe, private sector actors often tire of trying to understand how the Global Gateway functions in practice. It is not yet clear to many private sector actors, beyond the big equipment suppliers, how they can actually engage with and contribute to the Global Gateway, even when they have a strong interest in internationalisation. While ECAs are seen as a potential way to strengthen European private sector engagement, they are not necessarily familiar with the Team National and Team Europe approach.

Despite a willingness to work together, there are challenges to developing a truly effective Team Europe approach to connectivity. First steps in this direction have been taken, with the consolidation of the D4D Hub’s strategy in late 2024, which also set a more strategic direction for the Hub’s Connectivity working group. Yet, the challenge moving forward will be to build on the Team Nationals with a new approach to project development that allows a wider range of European member states and their private sector actors to contribute to the Tech Business Offer.

Conclusion and recommendations

Team Nationals are developing at varying speeds. Very different domestic institutional set-ups and resources complicate the process of combining national industrial strengths into a joint industrial offer. Team Europe has advanced considerably on the cooperation side, where hard infrastructure investments are reinforced by 'soft pillars', in which member state implementation agencies support capacity building, local regulations, and innovation ecosystems. Even stronger coordination and particularly information-sharing systems will be necessary to match the ambition of the EU tech business offer. There will also need to be more experimentation around how to work better together and develop joint projects. This is especially vital to smaller EU member states.

Building Team Nationals

-

Create authority and budget for Team National coordination. In many member states, key actors responsible for economic diplomacy, for development finance and for supporting innovation are located in separate ministries and have little or no interaction. In some cases, there continues to be mutual suspicion and even competition between ministries and their institutions. Member states should appoint senior Team National coordinators and give them sufficient authority and budget to coordinate effectively and incentivise joint programming and efforts. Although some Global Gateway ambassadors have been named, a more coordinated approach across the EU could add value.

-

Support key sub-sectors with national strengths. Member states should consider not only engaging with private sector representative bodies, but also selecting key sub-sectors on which to focus their Team Nationals. They should provide seed funding to support their internationalisation, with a strong focus on the role SMEs can play in tandem with larger players.

-

Use Team Nationals to identify SMEs for smart consortia. One European player alone may not be able to offer an end-to-end solution, but a consortium can fill this role. Well-organised Team Nationals can identify domestic manufacturers of key components or technology innovators and promote their inclusion in EU-wide smart consortia.

Building Team Europe

-

Make the Global Gateway Investment Hub much more user-friendly. The European Commission’s GG Investment Hub should transform its existing information interface into a user-oriented platform, which makes information readily available to MSs and their private sectors. Information sessions in national capitals could provide further support, as would the appointment of GG advisors in EC representations in the EU27. Member states, in turn, could better prepare their private sectors for international opportunities, including by better translating complex EU processes. The D4D Hub, through its interactions with representatives from Team Nationals and the European private sector, could support the implementation of the investment hub for digital sector-related projects.

-

Simplify coordination mechanisms. There is a need for a simpler process for identifying and scaling effective approaches from member states, and ensuring good coordination between relevant ministries, development agencies and financial institutions for development. Despite a clear willingness to work together, there are challenges for developing a truly effective Team Europe approach to ‘trusted connectivity’. The consolidation of the D4D Hub’s strategy in late 2024 and the more strategic direction being set for its Connectivity Working Group are a good start.

-

Create an effective information-sharing system. Either the European Commission or the D4D Hub should be given the mandate and sufficient resources to put in place an effective information-sharing system that would compile information on member state financing and cooperation projects in key geographies in order to give a more complete picture of Team Europe activities. This would go beyond GG flagships (so beyond the proposed GG Investment Hub), showcasing the breadth of European financing and cooperation on digital connectivity and beyond, sharing opportunities and putting in place mechanisms that encourage such cooperation between member states and their Team Nationals.

-

Pilot new mechanisms for building transnational consortia. This is vital to support small member states to play a role in the tech business offer, allowing companies from different Member states to co-develop bigger projects that integrate complementary expertise from across the EU.

Acknowledgements

The authors would like to thank Alberto Rizzi and Sasha Pearson for peer reviewing. We are also grateful to those who provided us with constructive feedback. In addition, we would like to thank Annette Powell and Joyce Olders for formatting support and Isabell Wutz for communications support. We are also deeply grateful to the many people who consented to be interviewed for this work.

The views expressed in this briefing note are those of the authors and do not necessarily represent those of ECDPM or any other institution. Any errors or omissions remain the responsibility of the authors. For comments and feedback, please contact Chloe Teevan (cte@ecdpm.org), Karim Karaki (kka@ecdpm.org) and Sabine Muscat (smu@ecdpm.org).

A full reference list is available in the PDF version of this brief.

Endnotes

1. Infranum represents 220 industrial companies, representing the entire digital infrastructure value chain, Sycabel comprises 20 energy and communication wires and cables industry manufacturers, French Telecommunications Federation (FFTélécoms) comprises 18 electronic communications operators in France, and the French Digital Industry Alliance (AFNUM) represents French manufacturers of: network and cloud equipment, IT and printing equipment, consumer electronics terminals, antennas, photography, and connected objects.