Opportunities for green ammonia fertiliser in East Africa

In this brief, Alfonso Medinilla, Koen Dekeyser and Francesco Rampa examine how green hydrogen and fertiliser production can act as a catalyst for green industrialisation and agricultural development in East Africa, highlighting how progress in one sector can help kick-start the other.

Summary

This brief examines how green hydrogen and fertiliser production can act as a catalyst for green industrialisation and agricultural development in East Africa, highlighting how progress in one sector can help kick-start the other.

Closing Africa’s yield gap and achieving food self-sufficiency – while also limiting land-use change – will not be possible without a significant scale-up in the application of mineral fertilisers. Locally produced and regionally traded green ammonia has the potential to address several of the current challenges related to import dependency and very high end-user prices.

While many challenges remain, a number of (green) fertiliser investments are underway. In the near term, domestic markets, shaped in large part by fertiliser input subsidy systems, as in Kenya, are likely to define the first phase of green fertiliser manufacturing in East Africa. However, real scale-up of African green fertiliser production and use will also depend on investments in regional market development and cross-border logistics, with a critical enabling role to be possibly played by the Northern Corridor. Doing so will require action on multiple fronts, linking agricultural modernisation with green energy, industrial policies and regional trade facilitation.

1. Introduction

This brief examines how green hydrogen and fertiliser production can act as a catalyst for African green industrialisation and agricultural development, highlighting how progress in one sector can help kick-start the other. It zooms in on recent developments in East Africa1, covering both large-scale fertiliser manufacturing and emerging decentralised production models, and explores how these interact with the political economy of fertiliser markets and input subsidy systems across the region. The note also examines the potential for regional fertiliser trade as a driver of green industrialisation and agricultural modernisation.

Closing Africa’s yield gap and achieving food self-sufficiency –while also limiting land-use change– will not be possible without a significant scale-up in the application of mineral fertilisers. East African agricultural systems depend completely on imports for all three key plant nutrients. As a result, farmers and public procurement agencies face some of the highest end-user fertiliser prices globally, particularly for urea, the most applied mineral fertiliser in East African farming systems. These high prices are driven by fossil fuel price volatility, currency depreciation, and persistent logistics inefficiencies.

Locally produced and regionally traded green ammonia has the potential to address several of these challenges simultaneously. It can help shield countries and farmers from external price shocks through partial import substitution, lower overall emissions by shifting new fertiliser production towards clean energy and green hydrogen as the main feedstock, and create new opportunities for industrialisation and large-scale energy investment across the region, while laying the groundwork for broader hydrogen-based industries. At the same time, it could form the basis for more integrated regional fertiliser markets and logistics efficiency gains, combining large-scale production hubs in Kenya (and potentially Ethiopia and Uganda) with decentralised, smaller-scale manufacturing solutions, particularly in Kenya and Ethiopia.

A number of fertiliser investments are underway, with three distinct models: large-scale green ammonia fertiliser in Kenya and Uganda, conventional grey urea manufacturing in Ethiopia and Tanzania, and efforts to develop and expand decentralised green ammonia production for use on large farms. Most of these initiatives are, for now, primarily national in scope, with Kenya’s geothermal-based green ammonia plans, closely linked to its national green hydrogen strategy, being the most advanced.

In the near term, domestic markets, shaped in large part by fertiliser input subsidy systems, as in Kenya, are likely to define the first phase of green fertiliser manufacturing in East Africa. However, real scale-up of African green fertiliser production and use will also depend on investments in regional market development and cross-border logistics. In this context, transport corridors such as the Northern Corridor, linking Kenya with Uganda, Rwanda and Burundi, and onward to the DRC, can play a critical enabling role in lowering costs and creating markets for locally produced green industrial goods. Doing so, however, will require action on multiple fronts, linking agricultural modernisation with green energy, industrial policies and regional trade facilitation.

2. East Africa could produce cheaper fertilisers

East African farmers today pay among the steepest fertiliser prices in the world. Import dependence, costly transport and taxes push up local prices for mineral fertilisers. In landlocked Uganda, urea –the most-used mineral nitrogen fertiliser– can be ten times more expensive than global prices. The impact is predictable: farmers apply too little. This has dire consequences. Under-application of fertiliser is a key reason yields lag, which pushes up food import bills and deepens rural poverty. Farmers often respond to low yields by clearing more land rather than boosting yields, accelerating deforestation, biodiversity loss and carbon emissions. A study across 21 African countries has even shown a positive correlation between urea prices and deforestation. High fertiliser prices also sap returns on investments, locking the region into a cycle of low-productivity production and environmental strain.

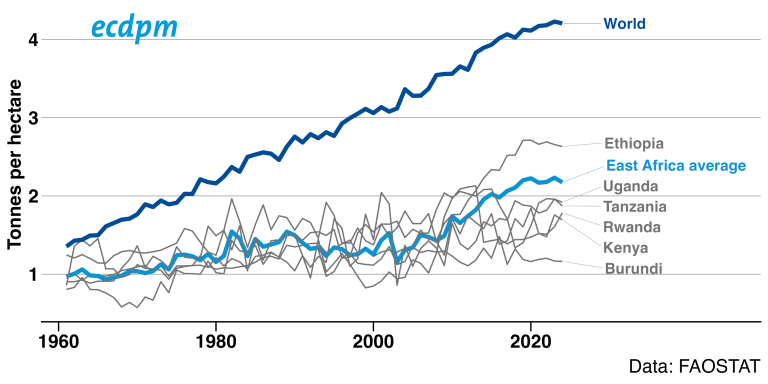

Fig. 1. Cereal yields in East Africa lag behind the rest of the world

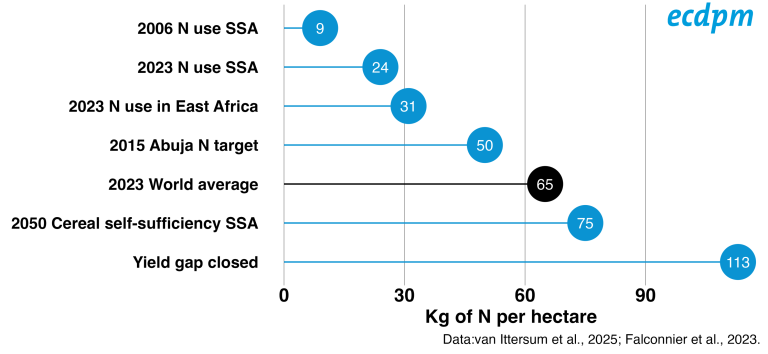

Unmet demand across East Africa is vast. Farmers apply on average 31 kg of nitrogen per hectare, compared to the (unmet) Abuja Declaration target of 50 kg and a global average closer to 65 kg (Fig. 2). With populations growing and diets shifting, the region will need far higher nutrient use simply to keep pace with demand. Closing the yield gap is essential to avoid ballooning food import bills and to meet rising consumption sustainably.

Fig. 2. How much nitrogen (N) is used and needed in sub-Saharan Africa?

East Africa today imports all its mineral fertiliser as no production happens in the region. Natural gas is the main energy input going into mineral nitrogen fertilisers, but –bar Tanzania and next-door Mozambique– no East African country is exploiting natural gas. This makes the whole region –except for limited Tanzanian phosphate– dependent on imports for all its fertilisers from a volatile and elevated international market, under upheaval due to the Russia-Ukraine war and high gas prices.

Green ammonia may offer a way out. Made from renewable electricity, water and air, it avoids the fossil-fuel dependence of conventional fertilisers and dramatically lowers emissions from producing them. Unlike traditional large-scale plants, green ammonia can also be produced in small-scale on-site units at large farms that then strip out part of the transport costs and could be especially interesting for low-infrastructure areas, yet it requires highly specialised skills to handle in its anhydrous form.

Price, however, remains a major challenge. As with all green hydrogen projects, green ammonia prices remain far from price parity with unabated fossil-fuel-based grey ammonia, and with natural gas prices stabilising since 2024, fully green mineral nitrogen fertilisers will continue to come at a premium compared to their conventional counterparts in the short to mid-term.

Yet the ‘Levelised Cost Of Hydrogen’ (LCOH), which is a plant’s average price for producing ammonia’s primary feedstock, a major cost, is only part of the picture. African farmers and distributors generally pay much higher prices than their counterparts in Asia and the Americas. One estimate is that imported mineral nitrogen prices at SSA ports between 2012 and 2022 were at least double those in the United States. High transport and transaction costs can account for half of the total fertiliser bill in some countries. At the same time, these persistent fertiliser price premiums imply that locally produced green ammonia can be more costly and still be competitive with lower-cost international producers, as long as a local ammonia sector can reduce logistics and distribution costs enough to achieve price parity at the farm gate.

3. Different business models for domestic fertiliser production

3.1 Fertiliser investment announcements are a mix of grey and green ammonia

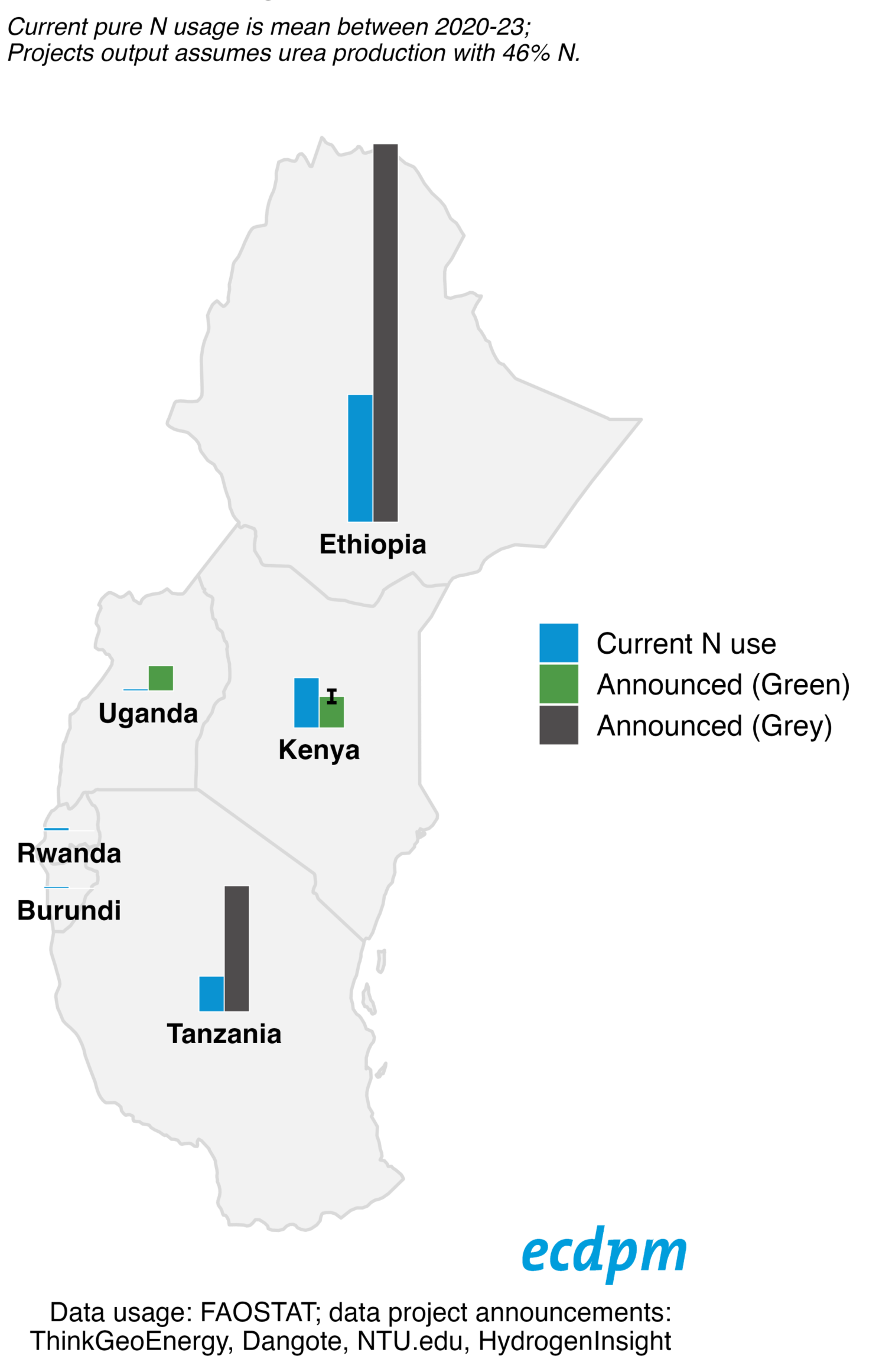

Several new fertiliser initiatives are underway across East Africa, spanning both large-scale and decentralised production models. These include large-scale and decentralised green ammonia projects in Kenya, large-scale - likely grey - urea plans by Dangote in Ethiopia, and proposals for large-scale green ammonia production in Uganda. The primary objective across all these initiatives is domestic import substitution.

Kenya is currently the most advanced case. The 2023 green hydrogen strategy and roadmap explicitly identify fertiliser as the most promising near-term application for green hydrogen. In November 2025, a groundbreaking ceremony was held for a green ammonia fertiliser plant in Kenya, representing a reported $800 million investment led by China’s Kaishan. The project aims to use 165 MW of geothermal power and is being developed in partnership with KenGen. It effectively revives earlier plans announced in 2022 by Fortescue Future Industries for a 300 MW facility, which reportedly failed to materialise due to the high cost of geothermal steam.

Kenya is also the only African country with an operational small-scale, modular ammonia plant. US-based Talus Ag has deployed containerised ammonia and fertiliser production at a large nut farm, producing around 200 tonnes of ammonia per year. The project reportedly achieves production costs equivalent to roughly 75% of the cost of imported fertiliser. It produces anhydrous ammonia, which is highly toxic and difficult to handle, requiring specialised equipment and skills to apply. This limits its suitability for small and medium-sized farms, which typically rely on granulated fertilisers using urea as their main nitrogen source. The company is, however, researching and developing alternative end products to better meet diverse market demand across Africa.

In Ethiopia, Dangote announced plans to develop a $4 billion urea factory in Gode, in the south-east of the country, with construction reportedly beginning in October 2025. The project is linked to parallel investments by China’s Golden Concord Group (GCL-Poly) in an oil refinery, which would provide a source of CO₂ for urea production, and in natural gas extraction, which would serve as the primary feedstock. The project is intended both to supply the domestic market and to position Ethiopia as a regional fertiliser exporter. In Tanzania, the Indonesian Essa Group announced a $1.3 billion investment for urea production near the southern city of Mtwara.

Uganda has also announced plans in recent years for a 100 MW green ammonia facility, developed with a Norwegian partner. Progress on this project seemed previously stuck on the lack of demand-improving policies and energy pricing, but in March 2026, an MoU was signed between the government, private sector, and development partners, signifying progress but still showing a long road towards implementation. This is similar to the bulk of African green hydrogen initiatives, which remain in the form of (often non-binding) project announcements. At present, none of the major fertiliser projects across the region has announced firm commissioning dates, and little is known about their financing structures or expected product pricing.

What is clear, however, is that these initiatives are primarily driven by domestic policy and political economy considerations, with limited explicit attention to regional market development or cross-border trade. If these projects come to their announced outputs - a big if - regional markets would be needed to absorb what the domestic market cannot, as announced output is more than current consumption. Ethiopian and Tanzanian announcements of grey urea production volumes are more than twice the current nitrogen use.

Kenya’s projected volumes of green ammonia could in theory be fully absorbed domestically. For green ammonia in particular, Kenya stands out as having a comparatively conducive policy and market framework. The country has a clear prioritisation of clean energy for green hydrogen development, alongside relatively well-established fertiliser market mechanisms. These include annual public procurement for input subsidies through the National Cereals and Produce Board, which purchases fertiliser from international suppliers; large and predictable private demand from commercial agriculture, notably through the tea sector; and multiple existing granulation and blending plants that could process domestically produced nitrogen and combine it with imported nutrients. Uganda, by contrast, appears the least advanced, with lower overall fertiliser demand and limited visible progress on green ammonia plans in recent years.

3.2 Towards a ‘thick’ and diverse nitrogen fertiliser market

While these business models differ, they are not mutually exclusive. Even under optimistic assumptions, projected production volumes from all announced projects would fall far short of potential fertiliser demand in East Africa (Fig. 2). Achieving food self-sufficiency or closing the yield gap across the sub-region would still require substantial imports, even if all current projects were to come online.

But East African farmers are likely to benefit from buying their nitrogen from a more diverse market, combining local, regional and international sources and different production technologies. This includes parallel development of large-scale, centralised green ammonia and fertiliser production, regional trade, and decentralised modular production models. Estimates suggest that modular electrolytic production could supply up to 40% of Africa’s nitrogen needs cost-effectively by 2030, once logistics premiums are taken into account. This is particularly the case if decentralised units can deliver lower-risk, user-friendly products suited to small and medium-sized farms. Such systems could supply clusters of farms in logistically challenging areas, help ease seasonal distribution bottlenecks, and may be particularly well suited to concessional climate finance aimed at accelerating deployment and reducing end-user prices.

Overall, there is a clear role for multiple business models in building a more resilient and competitive fertiliser market. At the same time, it is equally clear that supply-side investments alone will not be sufficient and will need to be matched by attention to market design, demand aggregation, and regional trade and logistics.

4. Thinking regionally: opportunities for cross-border fertiliser trade

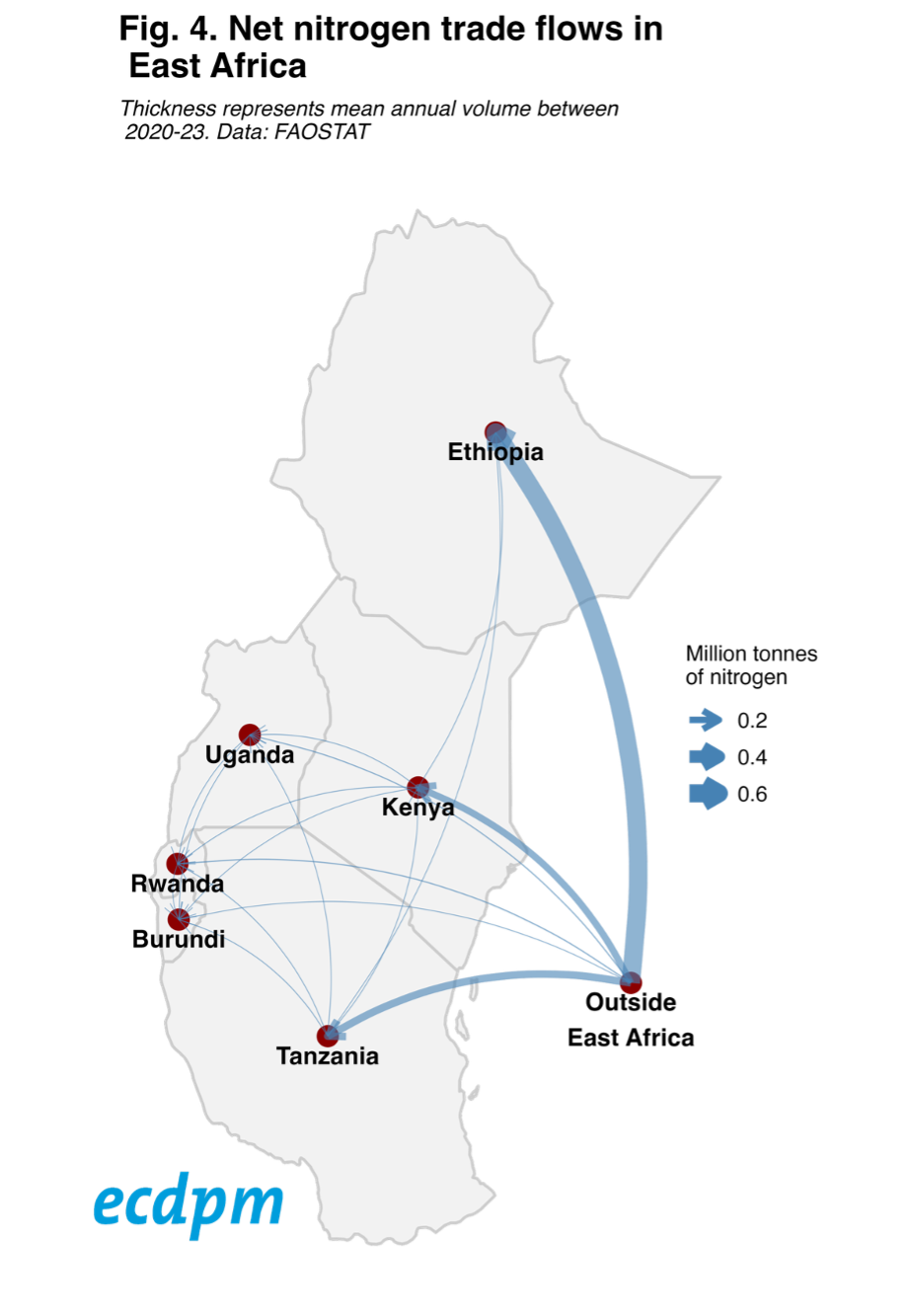

Fertiliser trade between Ethiopia and Kenya is a relatively recent development. Ethiopian imports from Kenya ramped up in 2024, with imports through the new Lamu port reflecting Kenya’s role as a regional fertiliser import and distribution hub. As a landlocked country and a major fertiliser consumer, Ethiopia arguably has the strongest incentive in the region to ramp up domestic production. In 2024, it was Africa’s largest fertiliser importer, with close to 2 million tonnes imported, of which more than 600,000 tonnes were nitrogen. Unlike Kenya, however, Ethiopia’s fertiliser re-exports are negligible.

Fertiliser trade between Ethiopia and Kenya is a relatively recent development. Ethiopian imports from Kenya ramped up in 2024, with imports through the new Lamu port reflecting Kenya’s role as a regional fertiliser import and distribution hub. As a landlocked country and a major fertiliser consumer, Ethiopia arguably has the strongest incentive in the region to ramp up domestic production. In 2024, it was Africa’s largest fertiliser importer, with close to 2 million tonnes imported, of which more than 600,000 tonnes were nitrogen. Unlike Kenya, however, Ethiopia’s fertiliser re-exports are negligible.

The Northern Corridor already sees a limited volume of mineral fertiliser trade. Kenya imported around 0.83 million tonnes of NPK, DAP, urea and CAN through its ports in 2024, and re-exported approximately 0.17 million tonnes, primarily to Uganda, Rwanda and Tanzania.

If Kenya can ramp up production of low-carbon nitrogenous fertilisers in a cost-effective way and leverage its existing mixing and granulation industry to meet specific demand from neighbouring markets, the corridor could act as a catalyst for investment in East African green ammonia. This could help bring down fertiliser prices across the region and enable agricultural modernisation that boosts yields, supports food security, and builds climate resilience.

While the theoretical business case is clear, it hinges on a number of crucial factors. These include demonstrating the potential for cost-competitive and predictable supply that can meet the seasonality of demand across different countries; balancing increased domestic production with reliable and affordable imports of other key nutrients; scaling up domestic and regional processing capacity to meet demand from neighbouring countries; and logistics interventions to enable higher seasonal volumes of bulk goods, including in some cases volatile or potentially hazardous substances such as ammonia.

Finally, price remains decisive. Persistently high fertiliser prices continue to dampen demand, particularly among small and medium-sized farmers, pushing application rates well below agronomic recommendations. Unless better markets can translate into lower and more stable end-user prices, opportunities will remain constrained.

5. Conditions for a regional market in East African green fertilisers

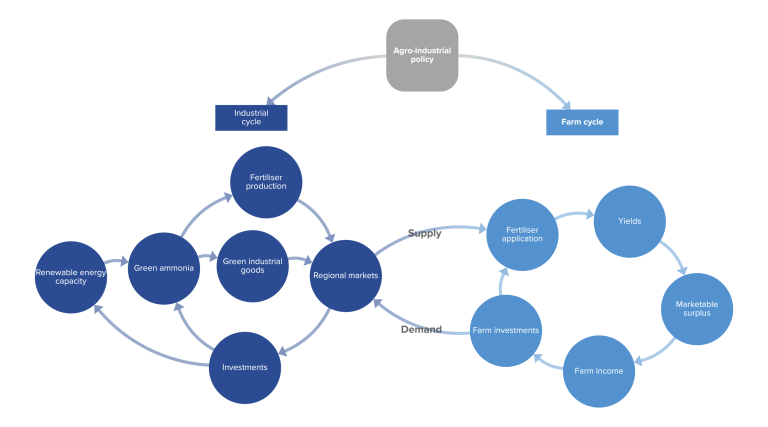

Green fertilisers offer a credible pathway to build domestic and regional lead markets for African green industrial goods. Beyond their relevance for industrial development, they deliver important co-benefits for food security by supporting yield increases and reducing pressure on biodiverse areas. Realising these opportunities, however, will require getting a set of enabling drivers right in the agricultural, financial, technical and logistical sectors:

-

Agricultural markets and policy: Nitrogen fertilisers are not a silver bullet for productivity gains. Yield increases depend on efficient and context-specific application, alongside farm and soil management and improved seeds. Price sensitivity and low market access remain core constraints on scaling both grey and green fertilisers, limiting the emergence of reliable domestic and regional markets.

-

Financial: The global green hydrogen sector is currently experiencing a correction phase, with project delays, rising financing costs and more cautious investment decisions slowing deployment. These challenges are amplified in African markets, where high capital intensity, infrastructure gaps and uncertainty offtake increase risk perceptions. Financing costs are likely to remain a major barrier to competitive green ammonia and fertiliser production.

Fig. 5. An agro-industrial policy is needed to connect the industrial and farm cycles with green fertilisers

3. Offtake: Ammonia could act as an important lead market for East African green hydrogen, but bringing prices down will require a more diverse set of offtakers - both in regional markets and different end-uses beyond fertilisers. Demand from e-fuels, bunkering and ammonia exports could provide scale and risk diversification, yet these markets remain highly uncertain and face significant financing and emerging competitor challenges.

4. Technical: Technical constraints further limit scalability. Ammonia’s toxicity and volatility create safety and handling challenges, which are particularly challenging for decentralised ammonia production: the fertilisers currently lack the granulated forms that small-holder farmers can use. Green urea production poses another specific challenge: while grey urea relies on CO₂ derived from its fossil-based ammonia production, green ammonia requires alternative CO₂ sources such as carbon capture or direct air capture, which remain costly and immature.

5. Logistics: Logistics and infrastructure are critical cost drivers. In East Africa, the Kenyan segment of the Northern Corridor, including the Standard Gauge Railway from Mombasa to Naivasha, plays a key role in moving bulk fertilisers inland, yet bottlenecks persist. Planned infrastructure expansions, including the extension of the SGR towards Uganda, could improve regional trade in fertilisers and inputs, including from Kenya’s own planned production facility near Naivasha. However, last-mile distribution, blending capacity and overall distribution efficiency will be decisive in reducing end-user costs and keeping public procurement expenditures in check.

Enabling these integrated drivers needs coordinated policy and financing approaches to create an enabling environment and wider demand. This includes thinking in terms of agro-industrial clusters, anchoring demand through procurement and aggregation mechanisms, and complementing large-scale supply-side investments with targeted support for research and innovation, modular ammonia solutions, sustainable urea pathways and alternative fertiliser products where industrial scale-up alone is insufficient.

A full reference list is available in the PDF version of this brief.

Endnotes

1. We have centred our scope on the Northern Corridor nations and neighbours: Ethiopia, Kenya, Tanzania, Uganda, Rwanda, and Burundi.

Our work on African food corridors

Explore our project page featuring ECDPM’s work on key African corridors, with insights on a variety of topics.